The conventional logic around digital banking goes something like this: evaluate carefully, modernize thoughtfully, don’t fall behind. It’s a reasonable starting point. But it undersells what’s actually at stake. While some banks and credit unions manage costs, others in your market are running on a Compounding Growth Platform that multiplies value year over year. The gap doesn’t hold steady. It accelerates.

The digital banking tech landscape

Your users are always comparing their current experience to that of every digital platform, from the neo-bank to the mega-bank, and even beyond banking to global consumer apps. And user expectations change rapidly.

Chase invested approximately $17 billion in technology last year1. Bank of America spent approximately $13 billion2. These figures represent weekly feature releases, continuously improving mobile experiences, and deepening data advantages over every other financial institution.

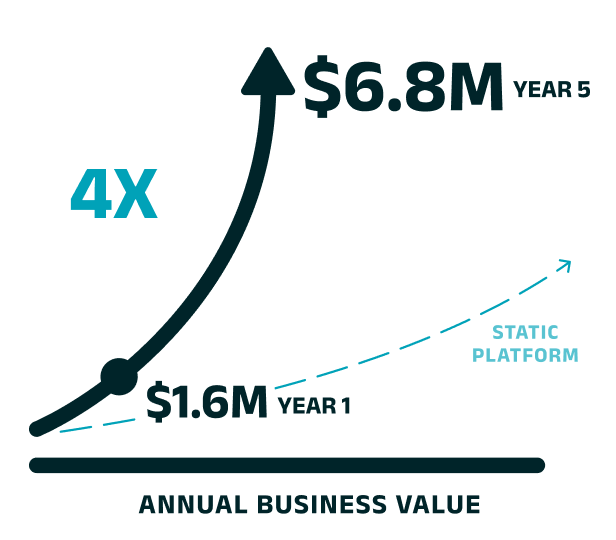

What compounding value actually looks like

A static platform maintains. A Compounding Growth Platform accelerates. The difference shows up slowly at first and then multiplies. During year one on a Compounding Growth Platform, an institution is still in its earliest growth phase: digital adoption is climbing, operational friction is falling, and early revenue signals are emerging. By year three, those signals have become structural advantages. By year five, the gap between that institution and one still running on a static platform isn’t a feature difference. It’s a trajectory difference and trajectories are very hard to reverse.

The ROI curve on a Compounding Growth Platform doesn’t flatten. It steepens.

Because every improvement to the platform builds on the one before it. Every engaged user generates data that makes the next campaign smarter. Every point of reduced churn compounds into retained relationships and deeper product penetration. The platform gets more valuable the longer an institution runs on it.

Five ways the gap compounds when your platform does not

The institutions not on a Compounding Growth Platform rarely experience a single dramatic failure.

User retention erodes quietly

Users drift toward institutions that have seamless experiences, one frustrating experience at a time. A platform that isn’t improving weekly is giving users a reason to look elsewhere, not dramatically, but consistently. Over five years, that quiet drift compounds into a meaningful retention gap.

Digital adoption plateaus

Active user rates on static platforms don’t climb, they stagnate. A Compounding Growth Platform gives users a reason to return. Each improvement deepens engagement, and deeper engagement drives the next improvement. That cycle doesn’t exist on a platform that ships four times a year.

Operational costs drift upward

Without self-service digital capabilities that work well, every user frustration becomes a call center ticket. Every clunky experience becomes a branch visit. Platforms that don’t improve continuously don’t reduce operational drag over time, they accumulate it.

Relationship depth stalls

Users on a Compounding Growth Platform are exposed to better, smarter, more contextually relevant experiences every time they log in. Products per relationship grow because the platform earns the right to offer them. On a static platform, cross-sell stays a campaign problem rather than a platform capability.

The competitive gap becomes structural

After three years, the advantage that compounding institutions have accumulated in data, intelligence, user depth, and operational efficiency isn’t a feature difference. It’s a structural one. Closing it requires more than just switching platforms. It requires years of compounding on a better platform to rebuild what was lost.

S&P Global Market Intelligence, Technology Impact on Business Report.

Based on a composite of Lumin Digital client deployments.

The cost of waiting is precisely calculable

Every quarter of waiting to switch, of vendor evaluation, is a quarter of compounding value not earned. Institutions that chose to compound their digital advantage three years ago are the ones breaking away in their markets today. Their users log in more frequently. Their commercial books are growing. Their NPS scores are at all-time highs. And their boards have stopped questioning the technology investment because the ROI is visible in every quarterly review.

The cost of not compounding isn’t hypothetical. It’s measurable and growing one quarter at a time, every year.

Source: 1JPMorgan Chase 2024 Investor Day presentation, May 2024. 2Bank of America 2024 Annual Report. Figures represent total firmwide technology spend and are not limited to digital banking platform investment.